A hypothetical open economy has a marginal propensity to import (MPI) equal to 0.2 and a marginal propensity to consume equal to 0.7 . Assume that the economy is initially in equilibrium. What will happen to the equilibrium real GDP if a tourist visits the country and spends $100 that she brought with her?

a. It will not change.

b. It will increase by $100.

c. It will increase by $200.

d. It will increase by $143.

e. It will increase by $90.

c

You might also like to view...

Market failures

A) prevent the price system from attaining economic efficiency. B) result in quantities and prices that are socially desirable. C) strengthen economic efficiency by forcing unprofitable firms to close. D) weaken the argument for government intervention in the economy.

If a person is taxed $1,000 on an income of $10,000 . taxed $2,000 on an income of $20,000 . and taxed $3,000 on an income of $30,000 . this person is paying a(n):

a. progressive tax. b. regressive tax. c. proportional tax. d. poll tax. e. excise tax.

When will a shortage occur in a market?

a. When the actual price is lower than the equilibrium price b. When quantity supplied is greater than the equilibrium quantity c. When the quantity that consumers are willing and able to purchase decreases d. When the quantity available at zero price is insufficient to meet demand e. When a price floor is set in the market

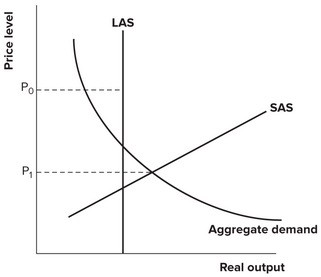

Refer to the graph shown. If the price level is P0, then:

A. both input prices and output will fall in the long run. B. both input prices and output will rise in the long run. C. input prices will fall and output will rise in the long run. D. input prices will rise and output will fall in the long run.