In the long run, for a perfectly competitive market, if economic profit is

A) less than zero, then some firms will exit the market and the market supply curve will shift leftward.

B) greater than zero, then some firms will enter the market and the market supply curve will shift rightward.

C) equal to zero, then there is no entry or exit of firms into or out of the market.

D) All of the above answers are correct.

D

You might also like to view...

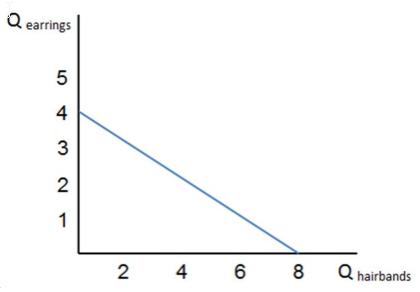

If the graph shown represents Tina's budget constraint, which of the following consumption bundles can Tina not afford?

A. Three pairs of earrings and four hairbands

B. Two pairs of earrings and four hairbands

C. No earrings and six hairbands

D. Cannot answer this question without knowing Tina's income and the prices of the two goods

What is productive efficiency? Does it guarantee that markets are operating efficiently?

Why is it rational for a consumer to begin buying a second type of good after buying a certain amount of the first type of good?

a. The price of the first type of good will continue to increase with each successive purchase. b. The total satisfaction gained from the first type of good will continue to decline with each successive purchase. c. The marginal satisfaction gained from the first type of good will continue to decline with each successive purchase. d. The price of the second type of good will continue to decrease with each successive purchase.

Refer to Table 21.3 below:Table 21.3Units of LaborUnits of OutputMPP00 1 30266 3 304116 What is the marginal physical product of the second unit of labor in Table 21.3?

A. 18. B. 36. C. 33. D. 66.