When labor is the variable input, the average product equals the:

A. quantity of output divided by the number of workers.

B. marginal product divided by the number of workers.

C. marginal product multiplied by the number of workers.

D. number of workers divided by the quantity of output.

Answer: A

You might also like to view...

Large countries can improve their welfare by levying a tariff only if it does not

A) encourage rent seeking elsewhere in the economy. B) discourage innovation. C) lead to retaliation by the nation's trading partners. D) All of the above. E) None of the above.

A perfectly inelastic demand curve exhibits

A) zero responsiveness to changes in price. B) zero quantity demanded when there is a slight change in price. C) a change in quantity demanded that is proportional to the change in price. D) a change in quantity demanded that is always twenty percent of the change in price.

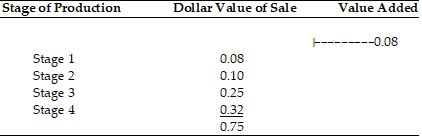

Refer to the above table. The production of this good has been through the first 3 stages of production. What is the total value added in Stage 1 through 3?

Refer to the above table. The production of this good has been through the first 3 stages of production. What is the total value added in Stage 1 through 3?

A. $0.75 B. $0.07 C. $0.43 D. Cannot be computed without more information.

Economic profits and losses are TRUE market signals because they

A) convey information in an asymmetrical fashion. B) convey information about rewards people should anticipate experiencing by shifting resources from one activity to another. C) convey information to public officials about where to encourage people to invest and what skills people should develop. D) cause people to move into careers in both undesirable and desirable industries with equal ease.