In the long run, economic profits are:

a. possible both for a monopolist and for a perfectly competitive firm.

b. possible for a monopolist but not for a perfectly competitive firm.

c. possible for a perfectly competitive firms but not for a monopolist.

d. impossible for both a monopolist and for a perfectly competitive firm.

b

You might also like to view...

In a demand-pull inflation, money wage rates rise because

A) a decrease in aggregate demand creates a labor shortage. B) an increase in aggregate demand creates a labor surplus. C) an increase in aggregate demand creates a labor shortage. D) a decrease in aggregate demand creates a labor surplus. E) an increase in aggregate supply creates a labor shortage.

Consider the following hypothetical difference-in-differences results concerning the average of hours worked in "big-box stores" between North and South Dakota before and after North Dakota increased its minimum wage. Average Weekly Hoursper Big-Box Establishment North Dakota South DakotaBefore ND minimum wage increase: 128.4 110.3 After ND minimum wage increase: 114.6 108.2 The minimum wage increase is associated with average hours of work decreasing by how much per week in North Dakota relative to South Dakota?

A. 20.2 hours B. 11.7 hours C. 2.1 hours D. 15.9 hours E. 13.8 hours

You are an efficiency expert hired by a manufacturing firm that uses K and L as inputs. The firm produces and sells a given output. If w = $40, r = $100, MPL = 20, and MPK = 40 the firm:

A. is profit maximizing but not cost minimizing. B. is cost minimizing. C. should use less L and more K to cost minimize. D. should use more L and less K to cost minimize.

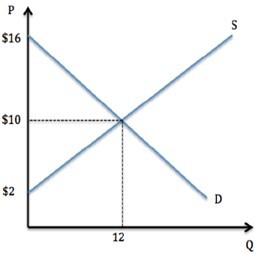

Assume the market was in equilibrium in the graph shown. If the market price gets set to $7, which of the following is true?

Assume the market was in equilibrium in the graph shown. If the market price gets set to $7, which of the following is true?

A. Some producers lose surplus, but total surplus rises. B. Some producers gain surplus, but total surplus falls. C. Some consumers lose surplus, but total surplus rises. D. Some consumers gain surplus, but total surplus falls.