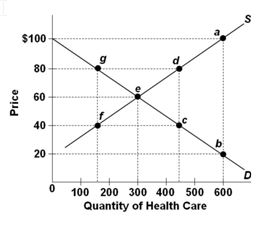

Refer to the below graph of a hypothetical market for health care. If there was not health insurance, the equilibrium price and quantity of health care would be:

A. $20 and 600 units

B. $40 and 450 units

C. $60 and 300 units

D. $80 and 450 units

C. $60 and 300 units

You might also like to view...

When an economist uses the term "cost" referring to a firm, the economist refers to the

A) price of the good to the consumer. B) explicit cost of producing a good or service but not the implicit cost of producing a good or service. C) implicit cost of producing a good or service but not the explicit cost of producing a good or service. D) opportunity cost of producing a good or service, which includes both implicit and explicit cost. E) cost that can be actually verified and measured.

In a market economy, buyers and sellers communicate their intentions to one another through:

a. government planners. b. negotiations overseen by government agencies. c. elected officials. d. prices.

Consumer surplus is what one consumer is willing to pay for a commodity over what another consumer is willing to pay for the same commodity

a. True b. False Indicate whether the statement is true or false

Producer surplus equals the

a. value to buyers minus the amount paid by buyers. b. value to buyers minus the cost to sellers. c. amount received by sellers minus the cost to sellers. d. amount received by sellers minus the amount paid by buyers.