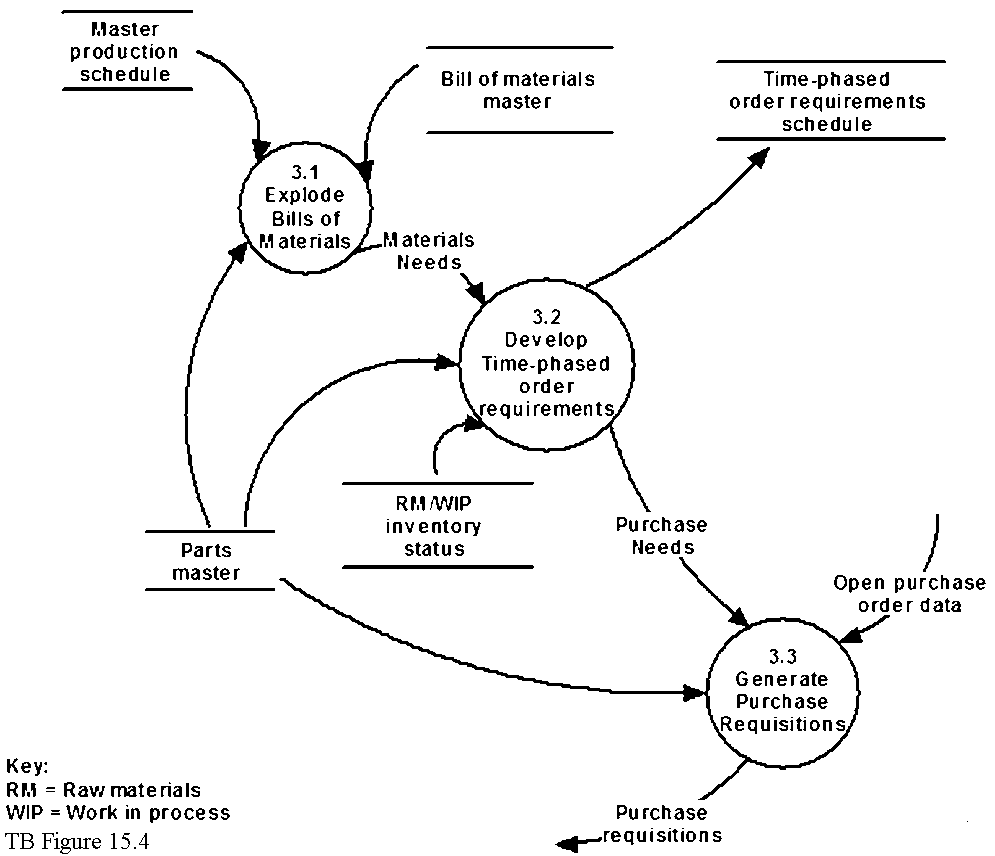

The process within TB Figure 15.3, Bubble 3.0 might be described as follows: After the master production schedule is determined, an important step in completing the production in a timely manner is identifying, ordering, and receiving materials. Materials requirements planning is a process that uses bills of material, raw material and WIP inventory status data, open order data, and the master

production schedule to calculate a time-phased order requirements schedule for materials and subassemblies. The schedule shows the time period when a manufacturing order or purchase order should be released so that the subassemblies and raw materials will be available when needed. The process involves working backward from the date production is to begin to determine the timing for manufacturing subassemblies and then moving back further to determine the date that orders for materials must be issued into the purchasing process. In an enterprise system, this process is performed automatically, using a variety of data from the enterprise database including:

•

Bills of materials, showing the items and quantities required as developed by engineering.

•

Parts master data, which contains information about part number, description, unit of measure, where used, order policy, lead time, and safety stock.

•

Raw materials and WIP inventory status data showing the current quantities on hand, and quantities already reserved for production for the materials and subassemblies.

•

Open purchase order data showing the existing orders fo

You might also like to view...

Which of the following best represents actions that may indicate fraud is pervasive throughout the company under audit?

a. The company's management negotiates deals with vendors in such a manner as to pay lower prices. b. The company's management drives luxury vehicles and takes vacations to exotic places. c. The company's management takes an overly aggressive approach to revenue recognition. d. The company's management estimates bad debts using an aged accounts receivables ledger rather than as a percent of sales.

Curvilinear costs increase as volume of activity increases, but at a nonconstant rate.

Answer the following statement true (T) or false (F)

Johnson Inc. owns control over Kaspar Inc. Johnson reports sales of $400,000 during 2018 while Kaspar reports $250,000. Kaspar transferred inventory during 2018 to Johnson at a price of $50,000. On December 31, 2018, 30% of the transferred goods are still held in Johnson's inventory. Consolidated accounts receivable on January 1, 2018 was $120,000, and on December 31, 2018 is $130,000. Johnson uses the direct approach in preparing the statement of cash flows. How much is cash collected from customers in the consolidated statement of cash flows?

A. $590,000. B. $635,000. C. $610,000. D. $625,000. E. $650,000.

If management perceives the current market equity value of their shares to be OVER valued, then management should:

A) issue new shares later after stock prices have come down so as not to further increase the price dilution found when issuing shares. B) issue new shares now to take advantage of the market mispricing, but only if they believe the market is at least momentarily inefficient. C) wait to issue until prices are UNDER valued so that there option values increase more rapidly. However, they would only do this if they have the best interest of shareholders in mind. D) recommend that existing shareholders buy more shares at current market prices because they are so valuable.