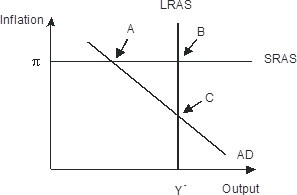

The economy pictured in the figure below has a(n) ________ gap with a short-run equilibrium combination of inflation and output indicated by point ________.

A. recessionary; B

B. recessionary; C

C. recessionary; A

D. expansionary; A

Answer: C

You might also like to view...

Many people argue against increasing the minimum wage because they believe the result would be increased unemployment. Which of the following best summarizes this argument? A higher minimum wage would

a. increase the supply of labor while decreasing the demand for labor b. decrease the supply of labor while increasing the demand for labor c. increase the quantity supplied of labor while decreasing the quantity demanded of labor d. decrease the quantity supplied of labor while increasing the quantity demanded of labor e. increase the supply of labor while decreasing the quantity demanded of labor

Several producers in industry A developed an improved technology that reduces the quantity of resources used to produce a given output. Which of the following would be expected?

a. The per-unit costs of production of the firms adopting the technology would increase. b. In the short run, economic profits would be earned by the earliest firms adopting the technology. c. Product price would immediately fall to the minimum average total cost of the firms quickly adopting the technology, thus retarding the rate at which firms enter the industry. d. Producers who adopt the technology will have short-run economic losses.

Frictional unemployment

a. can be created both by workers quitting to find more suitable jobs and changes in a country's comparative advantages. b. can be created by workers quitting to find more suitable jobs but not by changes in a country's comparative advantages. c. can be created by changes in a country's comparative advantages, but not by workers quitting to find new jobs. d. is not created by workers quitting to find more suitable jobs nor by changes in a county's comparative advantages.

In a perfectly competitive market,

a. one large firm controls the market and sets price, while the other smaller firms behave as price takers. b. all firms produce and sell a homogeneous product. c. the output sold by a particular firm may be quite different from the output sold by the other firms in the market. d. it's difficult for new firms to enter the market due to barriers to entry. e. the products sold by each firm are only slightly different.