As a firm expands output, in the short run marginal costs will

a. always decline as output expands.

b. increase at first but eventually level off and decline.

c. eventually increase as the firm experiences diminishing returns to the fixed factors of production.

d. initially increase at a decreasing rate but eventually increase at an increasing rate.

C

You might also like to view...

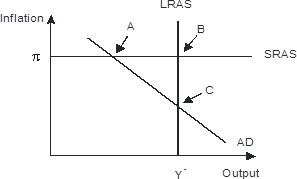

Refer to the figure below. In response to gradually falling inflation, this economy will eventually move from its short-run equilibrium to its long-run equilibrium. Graphically, this would be seen as

A. long-run aggregate supply shifting leftward B. Short-run aggregate supply shifting downward C. Aggregate demand shifting rightward D. Aggregate demand shifting leftward

The players in a two-person game are choosing between Strategy X and Strategy Y. If the second player chooses Strategy X, the first player's best outcome is also to select X. If the second player chooses Strategy Y, the first player's best outcome is to select X. For the first player, Strategy X is called a

a. dominant strategy b. collusive strategy c. tit-for-tat strategy d. repeated-trial strategy e. tacit strategy

Fluctuations in employment and output result from changes in

a. aggregate demand only. b. aggregate supply only. c. aggregate demand and aggregate supply. d. neither aggregate demand nor aggregate supply.

An increase in price causes exit from a constant-cost industry.

Answer the following statement true (T) or false (F)