What leads to a decrease in the quantity supplied of a good or service?

What will be an ideal response?

The quantity supplied of a good or service decreases when the price of the product decreases.

You might also like to view...

The ultimate objective of macroeconomics is to: a. reduce the unemployment rate in an economy

b. stabilize the growth rate in an economy. c. develop and test theories about how the overall economy works. d. improve the international competitiveness of U.S. financial markets. e. maximize the efficiency of government intervention in the marketplace.

At an output of one, variable cost is the same as __________.

Fill in the blank(s) with the appropriate word(s).

A constant-cost industry

A. is one in which an increase in demand is matched by a proportional increases in long-run supply. B. has a downward sloping long-run supply curve. C. generates increasing profits whenever demand increases because the new long-run equilibrium price is above the old price even though average costs have not changed. D. has a horizontal long-run supply curve.

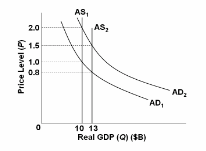

Answer this question on the basis of the diagram and the equation of exchange. Assume that the velocity of money is constant at 4. Suppose that the increase of aggregate supply from AS 1 to AS 2 indicates the economy's average increase in real output per year. According to monetarists, the proper monetary rule for price stability would be to increase the money supply by:

A. zero percent per year.

B. 4 percent per year.

C. 10 percent per year.

D. 30 percent per year.