When the government imposes an $8 price ceiling on a good that would have had a $10 equilibrium price without the ceiling,

A. surpluses are created.

B. supply will increase to meet the demand.

C. excess demand occurs.

D. quantity demanded of the good will fall.

Answer: C

You might also like to view...

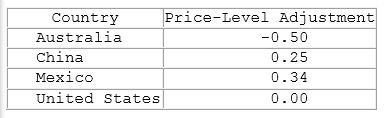

According to the table shown, if Bob is earning $30,000 in the United States and Bill is earning $40,000 in Mexico, what can be said about their standards of living?

This table shows the price-level adjustment as compared to the United States.

A. Bill is earning more in real terms than Bob.

B. Bob is earning more in real terms than Bill.

C. Bob and Bill are earning the same amount in real terms.

D. Bob and Bill are earning the same amount in nominal terms.

The price elasticity of demand for a product is a measure of the:

a. extent of competition in the market for the product. b. change in the quantity purchased of the product relative to a change in a consumer's income. c. change in the quantity demanded of the product due to changes in factors other than price. d. degree of consumer responsiveness to changes in the price of the product. e. percentage change in the prices of two related products.

Which of the following statements is true? a. Demand refers to how much of a good a consumer is willing to purchase at all prices

b. Demand refers to how much of a good a consumer is able to purchase at all prices. c. Demand refers to how much of a good a consumer is able to consume during a given period of time. d. Demand refers to how much of a good a consumer is willing and able to purchase at all prices.

If the production of capital goods is shown along the horizontal axis of a production possibilities curve, and the production of consumer goods is shown along the vertical axis of a production possibilities curve, and the economy desires to have a rapid

rate of economic growth, then the economy should produce at a point A) near the middle of the curve dividing resources equally between the production of consumer and capital goods. B) at a point near the vertical axis concentrating on the production of consumer goods. C) at a point near the horizontal axis concentrating on the production of capital goods. D) at a point inside the curve allowing the economy to adjust rapidly to changes in economic activity.