Under monopolistic competition, a long-run equilibrium exists when price equals:

A. marginal revenue.

B. minimum average total cost.

C. average total cost.

D. marginal cost.

Answer: C

You might also like to view...

If the demand for the Ford Mustang increases, we would expect Ford to

A) keep the price of Mustangs constant, regardless of the cost or benefit of a price change. B) increase the price of Mustangs to keep pace with the increase in demand. C) increase the price of Mustangs only if the benefit of a price increase outweighs the cost. D) decrease the price of Mustangs to maintain the increase in demand.

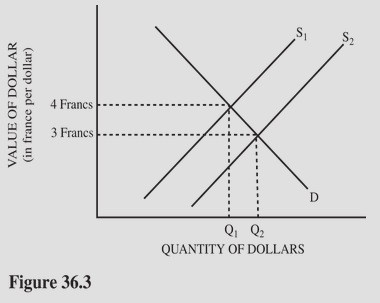

Suppose the supply of dollars increased from S1 to S2 in Figure 36.3. As a result of this change,

Suppose the supply of dollars increased from S1 to S2 in Figure 36.3. As a result of this change,

A. The Swiss franc will lose value worldwide. B. A trade surplus will be created in Switzerland. C. Swiss chocolate imports to the United States will be lower-priced. D. U.S. computer exports to Switzerland will be lower-priced.

Economic cost differs from accounting cost because accountants do not consider implicit costs.

Answer the following statement true (T) or false (F)

If total variable cost exceeds total revenue at all output levels, a perfectly competitive firm

A) should produce in the short run. B) is making short-run profits. C) should shut down in the short run. D) has covered its fixed cost.