Fixed costs are:

A. costs that depend on the quantity of output produced.

B. inputs costs that stay the same price per unit.

C. costs that don't depend on the quantity of output produced.

D. costs that are negotiated to stay the same throughout the life of a contract.

C. costs that don't depend on the quantity of output produced.

You might also like to view...

The government of a country decides it long-run exchange rate and intervenes regularly in the foreign exchange market to keep the exchange rate at its fixed level. The country is most likely to have a ________

A) fixed exchange rate system B) dirty-float exchange rate system C) real exchange rate system D) floating exchange rate system

Other things remaining the same, an increase in nominal GDP causes the velocity of money to:

a. Rise. b. Fall. c. Not change.

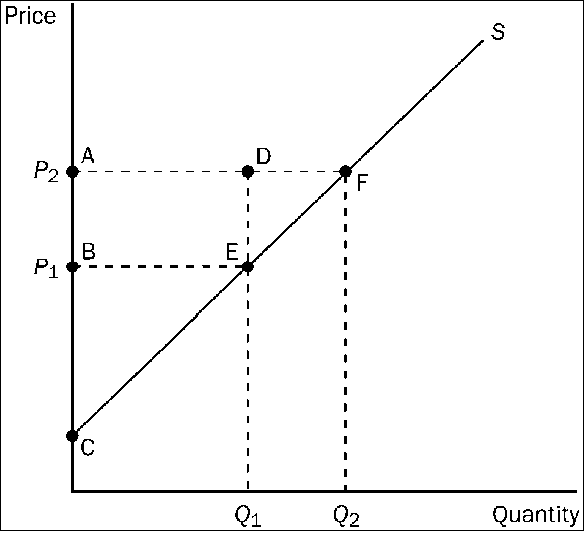

Figure 3-15

Refer to . Which area represents the increase in producer surplus when the price rises from P1 to P2 due to new producers entering the market?

a.

BCE

b.

ACF

c.

DEF

d.

AFEB

If the United States is operating at full production, not only are we using our most ________ technology, but we are utilizing our land, labor, capital and entrepreneurial ability at their most ________________.

Fill in the blank(s) with the appropriate word(s).