In a market that lacks sufficient competition,

a. output will generally be less than the output that is ideal from the standpoint of economic efficiency.

b. output will generally be greater than the output that is ideal from the standpoint of economic efficiency.

c. price will generally be less than the price that would result if the market was competitive.

d. profit rates will generally be so low that government subsidies will be necessary to ensure that the firms remain in business.

A

You might also like to view...

Your grandfather tells you that he earned $7,000/year in his first job in 1961. You earn $35,000/year in your first job in 2016. You know that average prices have risen steadily since 1961. You earn

A) more than 5 times as much as your grandfather in terms of real income. B) less than 5 times as much as your grandfather in terms of real income. C) less than 5 times as much as your grandfather in terms of nominal income. D) 5 times as much as your grandfather in terms of real income.

Which group believes that business cycles are unreal?

a. external cycle theorists b. internal cycle theorists c. real business cycle theorists d. housing cycle theorists e. innovation cycle theorists

In terms of purchasing power, the real minimum wage has ________ since 1997.

A. fallen B. stayed the same C. risen

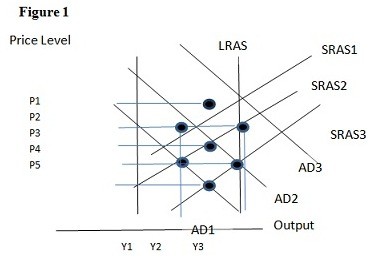

Using Figure 1 above, if the aggregate demand curve shifts from AD3 to AD2 the result in the short run would be:

A. P3 and Y1. B. P2 and Y1. C. P2 and Y3. D. P1 and Y2.