At an output of zero, total cost = ________________.

Fill in the blank(s) with the appropriate word(s).

fixed cost

You might also like to view...

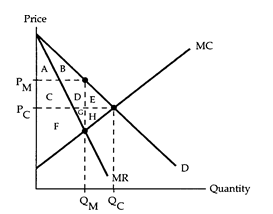

Refer to the market diagram. Of the surplus that consumers lose because there is a monopoly (and not perfect competition), how much is lost to the monopoly itself?

The following questions refer to the accompanying market diagram. PC and QC are the equilibrium price and quantity if the firm behaves competitively, and PM and QM are the equilibrium price and quantity if the firm is a simple monopoly.

a. Area C + D

b. Area E + H

c. Area A + B

d. Area C + D + E

Refer to Figure 5-8. Suppose the emissions reduction target is currently established at 8 million tons. Should society undertake to reduce an additional 1 million tons so that the total reduction is 9 million tons?

A) No, because there is a net cost represented by the area B + C. B) Yes, because toxic fumes are dangerous and must be eliminated at any cost. C) No, because the firms will pass the additional cost on to consumers. D) Yes, because the marginal benefit exceeds the marginal cost at 8 million tons.

Sally’s Sweaters operates in a perfect competition market. This means Sally faces which of the following?

a. Many competitors and is a price taker b. Many competitors and is a price setter c. Few competitors and is a price taker d. Few competitors and is a price setter

A political opponent argues that unemployment insurance is bad for the economy. How would you counter this argument to show that unemployment insurance is actually good for the economy?

What will be an ideal response?