Assume the production technology changes for a good that is currently produced in a perfectly competitive market

In particular, the new technology is such that the marginal costs of production for a single firm decline over the entire range of the demand curve for the good in question. How would this affect the number of firms that operate in this market? Explain.

Eventually, one firm would control the entire market. This would result from increases in capacity by firms attempting to lower costs and therefore earn economic profits in the short run. Firms that expand would be able to sell their output at a lower price and still earn a normal profit (or possibly economic profit). Other firms would be forced to expand or leave the market. Expansion of plant capacity by some firms and exit by others would continue until only one firm was left in the market.

You might also like to view...

Forty or so dealers establish a "market" in these securities by standing ready to buy and sell them

A) secondary stocks B) surplus stocks C) U.S. government bonds D) common stocks

Which of the following policies is likely to generate the smallest increase in national saving?

A) an increase in income taxes B) an increase in consumption taxes C) a cut in government transfer payments D) None of the above policies will increase national saving.

In what way does monopolistic competition favor consumers?

A) A limited number of sellers differentiate their products or services by offering better quality items and/or greater incentives to purchase them. B) A large number of sellers providing virtually identical products means that no single seller can set the price. C) A large number of sellers and products increases supply of similar, but not identical, products and services, so to increase demand sellers are likely to reduce prices. D) A single seller or provider ensures consistency of product quality and regulated pricing. E) A large number of sellers of virtually identical products means that no single seller can set the price for these products.

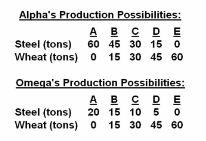

Refer to the given data. Alpha is a(n):

A. increasing-cost economy, whereas Omega is a constant-cost economy.

B. constant-cost economy, whereas Omega is an increasing-cost economy.

C. increasing-cost economy, as is Omega.

D. constant-cost economy, as is Omega.