Answer the following questions true (T) or false (F)

1. If in the long run a firm makes zero economic profit, it should exit the industry.

2. A perfectly competitive firm in a constant-cost industry produces 1,000 units of a good at a total cost of $50,000. If the prevailing market price is $48, the number of firms and the industry's output will decrease in the long run.

3. Suppose there are economies of scale in the production of a specialized memory chip that is used in manufacturing microwaves. This suggests that the microwave industry is a decreasing-cost industry.

1. FALSE

2. TRUE

3. TRUE

You might also like to view...

Refer to the scenario above. If they are the only bidders in the auction and each bidder uses his optimal strategy, the maximum price the winner is likely to pay is ________

A) $210 B) $350 C) $500 D) $625

Economists Eichengreen and Hausmann coined the phrase original sin to describe developing countries inability to borrow in their own currencies. Where do they believe that this inability comes from? What are other beliefs on this topic?

What will be an ideal response?

National defense and coastal lighthouses are examples of

a. public goods. b. private goods. c. high marginal cost goods. d. depletable goods.

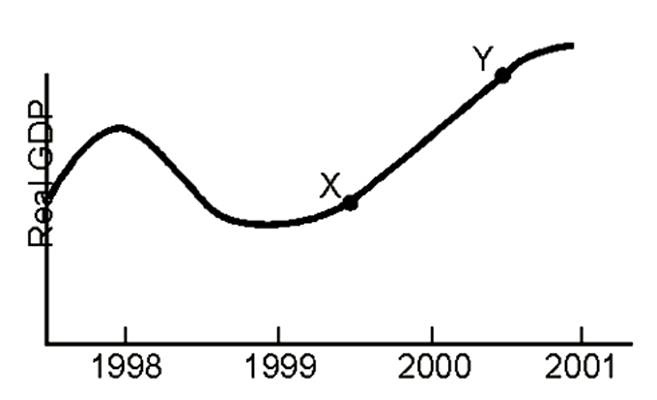

Point Y is in the _____ phase of the business cycle.

A. prosperity

B. recovery

C. depression

D. recession