The GDP of an economy is equal to the sum of the values of its consumption expenditure, investment expenditure, government expenditure, exports, and imports

a. True

b. False

Indicate whether the statement is true or false

False

You might also like to view...

The nature of a firm's cost (fixed or variable) depends on the

a. firm's revenues. b. time horizon under consideration. c. price the firm charges for output. d. explicit but not implicit costs.

A decrease (leftward shift) in the supply for a good will tend to cause

a. an increase in the equilibrium price and quantity b. a decrease in the equilibrium price and quantity c. an increase in the equilibrium price and a decrease in the equilibrium quantity d. a decrease in the equilibrium price and an increase in the equilibrium quantity e. none of the above.

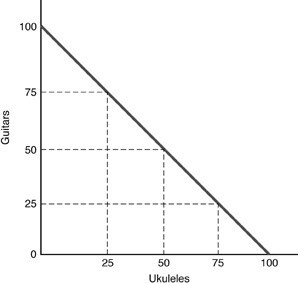

In the above figure, as more ukuleles are produced, the opportunity cost in terms of guitars is

In the above figure, as more ukuleles are produced, the opportunity cost in terms of guitars is

A. decreasing. B. increasing. C. zero. D. constant.

A permanent reduction in net exports leads to

A. a proportional increase in real Gross Domestic Product (GDP). B. a more than proportional decrease in real Gross Domestic Product (GDP). C. a reduction in taxes, autonomous government spending, and a fall in real Gross Domestic Product (GDP). D. a less than proportional decrease in real Gross Domestic Product (GDP).