The total cost of production is determined by adding the costs of which of the following?

A. Labor, capital, land, intermediate inputs, and business know-how

B. Labor, capital, land, and revenue

C. Labor, capital, revenue, and marginal product

D. Business know-how, capital, and land

Answer: A

You might also like to view...

The data in the table above shows the consumption by families in a small (poor) economy. The families consume only salt and bread. The reference base period is 2011. The cost of the CPI market basket in 2011 is

A) $64.00. B) $3.50. C) $52.00. D) $5.00. E) $100.

If Congress instituted an investment tax credit, the equilibrium quantity of loanable funds would

a. rise. b. fall. c. be unchanged. d. move in an uncertain direction.

Treasury Bonds are

a. both a store of value and a medium of exchange. b. a store of value, but not a medium of exchange c. a medium of exchange, but not a store of value. d. neither a store of value nor a medium of exchange.

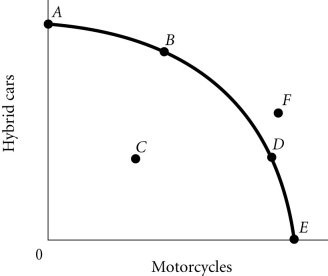

Refer to the information provided in Figure 2.4 below to answer the question(s) that follow. Figure 2.4According to Figure 2.4, as the economy moves from Point A to Point E, the opportunity cost of motorcycles, measured in terms of hybrid cars

Figure 2.4According to Figure 2.4, as the economy moves from Point A to Point E, the opportunity cost of motorcycles, measured in terms of hybrid cars

A. remains constant. B. decreases. C. initially increases, then decreases. D. increases.