It is not true in the long run of monopolies that

A. other firms seeking positive economic profit enter the market.

B. they earn positive economic profit.

C. they sell their output at a price greater than marginal cost.

D. they benefit from barriers to entry.

Answer: A

You might also like to view...

How does the principal-agent problem extend to managers and employees?

What will be an ideal response?

Consider the following: there are two countries, A and B. Each country has the same resources, and produces the same goods. The residents of country A use money; the residents of country B rely on bartering of goods. Will each country produce the same quantity of output? Explain.

What will be an ideal response?

Which statement is an economic rationale for the law of increasing opportunity cost?

A. The economy is employing all of its available resources. B. Many economic resources are better at producing one product than another. C. The economy is achieving productive efficiency by producing goods and services at the least cost. D. In any economy, the state of technology is changing and resources are variable.

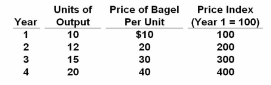

Refer to the data. Real GDP in year 4 is:

A. $320.

B. $450.

C. $200.

D. $800.