Final sales plus changes in inventories equals GDP.

Answer the following statement true (T) or false (F)

True

You might also like to view...

Suppose a Cournot oligopoly is operating in a market where demand is linear and marginal costs are constant. We can conclude that the total output supplied is

a. 1/3 of the perfectly competitive output. b. 1/2 of the perfectly competitive output. c. 2/3 of the perfectly competitive output. d. equal to the competitive output.

Refer to the above figure. Suppose the original long-run equilibrium was at point B. What could have caused the move to the current equilibrium?

A) Aggregate demand must have decreased. B) Input prices must have increased, causing long-run aggregate supply to increase. C) Decreases in the price level caused short-run aggregate supply to fall. D) A temporary reduction in production due to bad weather.

Suppose that the inverse demand for a downstream firm is P = 150 ? Q. Its upstream division produces a critical input with costs of CU(Qd) = 5(Qd)2. The downstream firm's cost is Cd(Q) = 10Q. When there is no external market for the downstream firm's critical input, the marginal revenue for the downstream firm is:

A. MRd(Q) = 140 ? Q. B. MRd(Q) = 150 ? 2Q. C. MRd(Q) = 150 ? Q. D. MRd(Q) = 140 ? 2Q.

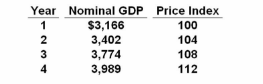

Answer the question based on the following data, using year 1 as the base year. All dollars are in billions.

Refer to the above data. Real GDP increased from year 3 to year 4 by approximately:

A.

$68 billion

B.

$75 billion

C.

$98 billion

D.

$215 billion