If there is an increase in the demand for a good, what will happen to the equilibrium price and quantity of the good exchanged?

a. Decrease Decrease

b. Increase Decrease

c. Decrease Increase

d. Increase Increase

d. Increase Increase

You might also like to view...

The market demand curve is derived by summing individual demand curves horizontally

a. True b. False Indicate whether the statement is true or false

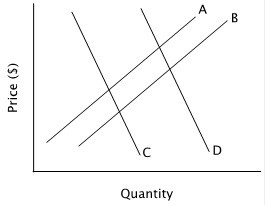

Refer to the figure below. An increase in supply is represented by a shift from:

A. curve C to curve B. B. curve A to curve B. C. curve B to curve A. D. curve C to curve D.

A farm is able to produce 5,000 bushels of peaches per season on 100 acres. Assume it adds one more acre and is able to produce 6,000 bushels per season. The marginal product of the additional acre of land for this farm is:

A. 6,000 bushels per acre per year. B. 5,000 bushels per acre per year. C. 1,000 bushels per acre per year. D. 11,000 bushels per acre per year.

What is the law of diminishing marginal product?

What will be an ideal response?