If the marginal cost of producing the next unit of output is less than the average total cost, then:

A. the average total cost curve is increasing.

B. the marginal cost curve is at its minimum.

C. the average total cost curve is decreasing.

D. the average total cost curve is at its minimum.

Answer: C

You might also like to view...

When the expected inflation rate changes, what happens to the short-run Phillips curve? To the long-run Phillips curve?

What will be an ideal response?

In a perfectly competitive market

A. if a firm raises its price, it will lose some, but not all, of its customers. B. when a firm sells another unit of output, the addition to total revenue is equal to market price. C. a firm faces a perfectly elastic demand because there is unrestricted entry and exit. D. all of the above E. none of the above

In the long run:

A. all factors of production are fixed. B. all factors of production are variable. C. some factors of production are variable, while at least one factor of production is fixed. D. None of these are correct.

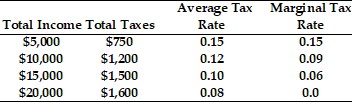

Refer to the information provided in Table 19.1 below to answer the question that follows.

Table 19.1  Refer to Table 19.1. The tax rate structure in this example is

Refer to Table 19.1. The tax rate structure in this example is

A. proportional. B. progressive. C. regressive. D. marginal.