The process of entry and exit into a monopolistically competitive market continues until:

A. profits are zero.

B. long-run equilibrium is reached.

C. price is equal to average total cost.

D. All of these statements are true.

D. All of these statements are true.

You might also like to view...

Figure 11-2

?

In Figure 11-2, which of the points are efficient allocations of resources?

In Figure 11-2, which of the points are efficient allocations of resources?

A. A, B, and C B. B and C only C. C and B and D D. B only

In competitive markets, buyers

a. are price takers, but sellers are price setters. b. are price setters, but sellers are price takers. c. and sellers are price takers. d. and sellers are price setters.

Change in Supply

What will be an ideal response?

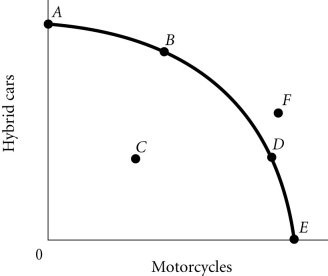

Refer to the information provided in Figure 2.4 below to answer the question(s) that follow. Figure 2.4According to Figure 2.4, as the economy moves from Point A to Point E, the opportunity cost of motorcycles, measured in terms of hybrid cars

Figure 2.4According to Figure 2.4, as the economy moves from Point A to Point E, the opportunity cost of motorcycles, measured in terms of hybrid cars

A. remains constant. B. decreases. C. initially increases, then decreases. D. increases.