What is a gold standard?

What will be an ideal response?

A gold standard is a monetary system in which gold backs up paper money. In a traditional gold standard, a person can present paper money to the government and receive its stated value in gold.

You might also like to view...

An international agency uses the prices of iPads in different countries to compute the exchange rate between the currencies of these countries. Which of the following measures is based on a similar idea?

A) The midcap index B) The Human Development Index C) The Big Mac Index D) The GDP deflator

If the price elasticity of demand for gasoline is 0.8 and the price elasticity of demand for plane tickets is 2.2 then the demand for gasoline is ________ and the demand for plane tickets is ________

A) elastic; inelastic B) inelastic; elastic C) elastic; elastic D) inelastic; inelastic

If the demand curve is a downward sloping straight line, the price elasticity of demand always

A) increases as the demand curve shifts rightward. B) increases as the demand curve shifts leftward. C) increases with movements upward along the demand curve. D) decreases with movements upward along the demand curve.

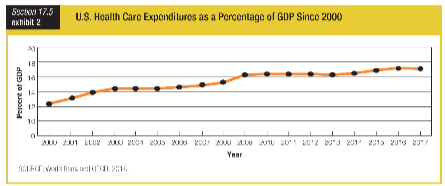

Based on the graph showing U.S. health care expenditures as a percentage of GDP, during which period did health care expenditures rise the most?

a. 2002 to 2006

b. 2006 to 2009

c. 2009 to 2013

d. 2013 to 2016