The value of the marginal product of any input is equal to the marginal product of that input multiplied by the

a. wage.

b. marginal cost of the output.

c. change in total profit.

d. market price of the output.

d

You might also like to view...

Las Vegas Sands Corporation is trying to acquire 50 acres of land to build a casino resort in Pennsylvania. There are 60 houses on the land the company needs

Explain how eminent domain could be beneficial in the process of acquiring this land in terms of transactions costs and the holdout problem.

The phrase "double coincidence of wants" ________

A) is useful to explain why barter is an efficient practice B) refers to two people who have similar tastes C) suggests a quite improbable circumstance D) clarifies the distinction between income and wealth E) none of the above

The difference between producer surplus and profit is always the associated with

A) opportunity costs. B) total costs. C) variable costs. D) fixed costs.

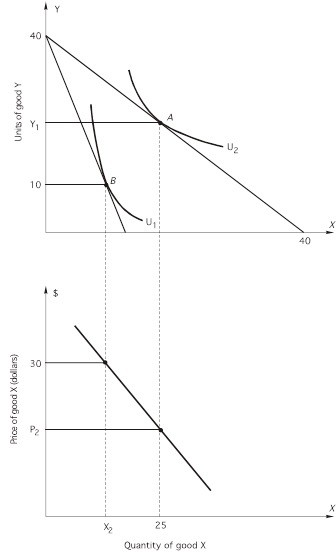

According to the following graphs, what is Y1? The price of Y is $15 per unit.

The price of Y is $15 per unit.

A. 20 B. 12 C. 25 D. 15 E. none of the above