A competitive market is in equilibrium. Then there is a decrease in demand and a decrease in supply. The equilibrium price ________, and the equilibrium quantity ________

A) rises; decreases

B) perhaps changes but we can't say if it rises, falls, or stays the same; decreases

C) falls; increases

D) perhaps changes but we can't say if it rises, falls, or stays the same; increases

E) rises; increases

B

You might also like to view...

Compared to the pay increase from just a third year of college, the actual pay increase resulting from a fourth year that results in graduation is

a. several times smaller b. the same c. only very slightly greater d. several times greater e. No economist has ever studied this issue

Scarcity is the result of:

a. government decision making b. inappropriate normative judgments. c. positive economics. d. wants that exceed the resources necessary to provide them.

If the marginal propensity to consume is 0.75 and autonomous consumption spending will decrease by $30 billion, by how much would net taxes need to decrease in order to have no change in output? (Ignore any timing issues.)

a. $60 billion b. $30 billion c. $90 billion d. $120 billion e. $40 billion

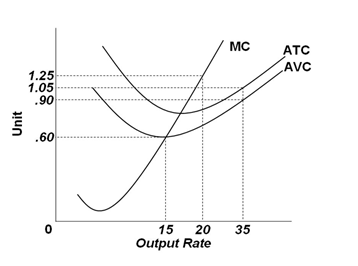

Refer to the graph below. It shows the cost curves for a competitive firm. If the market price falls to $0.55, the optimal output rate is:

A. 0

B. 15

C. 20

D. More than 20, but less than 35