We measure a person's productive contribution in a market system by

A) the marginal factor cost theory of the firm.

B) the profit maximization theory of the firm.

C) the marginal revenue product theory of wage determination.

D) the egalitarian theory of wage determination.

Answer: C

You might also like to view...

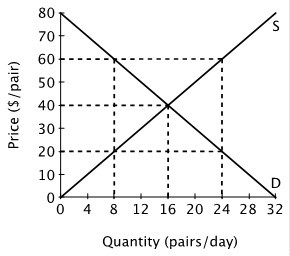

The figure below shows the supply and demand curves for jeans in Smallville.  At the price of $60 per pair, sellers offer _____ pairs of jeans per day, and buyers wish to purchase ________ pairs of jeans a day.

At the price of $60 per pair, sellers offer _____ pairs of jeans per day, and buyers wish to purchase ________ pairs of jeans a day.

A. 8; 24 B. 16; 16 C. 24; 8 D. 60; 20

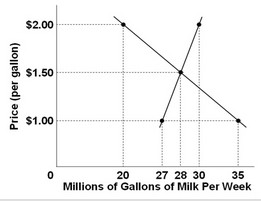

Use the following graph of the market for milk to answer the question below. In this market, the equilibrium price is ________ and equilibrium quantity is ________.

In this market, the equilibrium price is ________ and equilibrium quantity is ________.

A. $28 per gallon; 150 million gallons B. $1.50 per gallon; 30 million gallons C. $1.50 per gallon; 28 million gallons D. $1.00 per gallon; 35 million gallons

When both players in a zero-sum game play their ideal strategies, the expected payoff for each player is zero

Indicate whether the statement is true or false

If there is an improvement in technology that affects only Aggregate Supply and a nation's wealth falls due to sagging stock market, then:

a. Aggregate demand rises, and aggregate supply falls. b. Aggregate demand and aggregate supply rise. c. Aggregate demand and aggregate supply fall. d. Neither aggregate demand nor aggregate supply change. e. Aggregate demand falls, and aggregate supply rises.