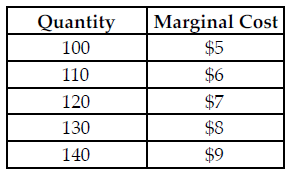

Refer to the table below. The perfectly competitive firm has a random demand with a 50 percent chance of being $5 and a 50 percent chance of being $7. What quantity should the firm produce to maximize its expected profit?

The above table summarizes the marginal cost of production at various quantity levels for a perfectly competitive firm.

A) 110

B) 120

C) 100

D) 130

A) 110

You might also like to view...

The above figure shows the apartment rental market in Bigtown. At what rent will there be neither a shortage nor a surplus of apartments?

A) $1250 per month B) $1000 per month C) $750 per month D) $500 per month

If, due to a recession, foreign workers begin to leave the United States to search for temporary work in their home countries until the recession has ended, this will

A) move the home country's economy up along a stationary short-run aggregate supply curve. B) shift the short-run aggregate supply curve of the home country to the left. C) shift the short-run aggregate supply curve of the home country to the right. D) move the home country's economy down along a stationary short-run aggregate supply curve.

Which of the following is true?

A) Changes in personal costs and benefits will exert a predictable influence on the choices of people. B) If the intentions behind a policy are good, you can be assured that the outcome will be desirable. C) If a good is provided free to an individual by government, its production will not consume valuable scarce resources. D) If one individual gains from an economic activity, then someone else must lose.

If the demand for a product decreases by 16 percent, the supply elasticity is 1.2, and demand elasticity is 0.80, then the equilibrium price will decrease by 6 percent.

Answer the following statement true (T) or false (F)