In the monopoly market structure, new firms

a. cannot profitably enter the industry, even in the long run

b. may freely enter and leave the industry in both the short run and the long run

c. may freely enter and leave the industry in the long run only

d. may freely enter and leave the industry in the short run only

e. have no incentive to enter the industry, even if economic profits are present

A

You might also like to view...

Classical economists believe that:

a. velocity is not constant. b. changes in the money supply affect real GDP. c. the quantity of money explains prices. d. the money supply affects velocity.

Every Friday night Elizabeth either goes bowling or goes to the movies. Because the price of bowling went up, Elizabeth now sees more movies. Elizabeth's behavior would be best described as a change in which determinant of demand?

a. Price of complementary goods b. Expectations c. Income d. Number of buyers e. Price of substitute goods

Suppose a country, whose production and consumption of coffee is large relative to the world market, has just entered the global market. If the country is a net exporter of coffee, we would expect:

A. a decrease in world price, and increase in world quantity of coffee. B. an increase in both world price and quantity of coffee. C. an increase in world price and decrease in world quantity of coffee. D. a decrease in both world price and quantity of coffee.

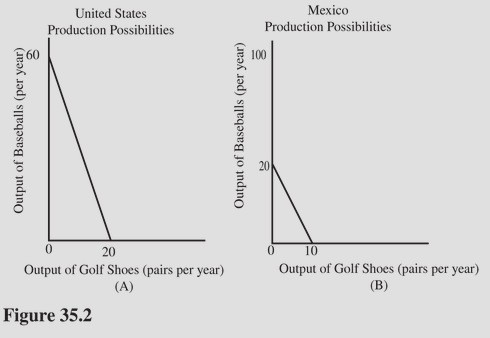

The production possibilities curves illustrated in Figure 35.2 reveal that

The production possibilities curves illustrated in Figure 35.2 reveal that

A. The United States has no comparative advantage. B. The United States has an absolute advantage in both goods. C. Mexico has a comparative advantage in baseballs. D. Mexico has no comparative advantage.