If demand decreases and supply increases, price will

a. always increase

b. always decrease

c. increase only if supply increases more than demand decreases

d. increase only if supply increases less than demand decreases

e. decrease only if supply increases more than demand decreases

B

You might also like to view...

Opportunity cost is best defined as:

a. the sum of all alternatives given up when a choice is made. b. the money spent once a choice is made. c. the highest-valued alternative given up when a choice is made. d. the difference between the cost price and the selling price of a good. e. the cost of capital resources used in the production of additional capital.

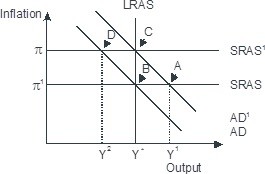

Based on the figure below. Starting from long-run equilibrium at point C, a tax increase that decreases aggregate demand from AD1 to AD will lead to a short-run equilibrium at point ________ and eventually to a long-run equilibrium at point ________, if left to self-correcting tendencies.

A. D; C B. D; B C. A; B D. B; C

Exhibit 9-5 Demand and cost data for a monopolist Price Quantity TR MR TC Profit $10 1 10 10 4 9 2 8 8 3 12 7 4 16 6 5 20 5 6 24 4 7 28 3 8 32 2 9 36 1 10 40 Refer to Exhibit 9-5. The demand schedule and cost schedule for a monopolist are provided. Which output level maximizes profit?

A. 2. B. 6. C. 4. D. 7.

Answer the question based on the following price and output data over a five-year period for an economy that produces only one good. Assume that year 2 is the base year.YearUnits of OutputPrice Per Unit18$22103315441855206If year 2 is the base year, the real GDP for year 3 is:

A. $45. B. $60. C. $40. D. $30.