Suppose the savings rate is 15 percent. For every dollar the government collects in tax revenue and spends on public goods and infrastructure, the net result will be _____.

(A) An increase in total investment by 85 cents.

(B) A decrease in total investment by 15 cents.

(C) An increase in total investment by 15 cents.

(D) No change in the total investment.

Ans: (A) An increase in total investment by 85 cents.

You might also like to view...

Suppose a jar of orange marmalade that is ultimately sold to a customer at The Corner Store is produced by the following production process: Name of CompanyRevenuesCost of Purchased inputsCitrus Growers Inc.$0.750Florida Jam Company$2.00$.75The Corner Store$2.50$2.00What is the sum of the value added of all the firms?

A. $4.50 B. $2.50 C. $5.25 D. $2.75

Answer the following statement(s) true (T) or false (F)

1. A volume-based effluent fee is based on the degree of harm linked to the contaminant released. 2. Polluting sources have an incentive to abate up to the point where their Marginal Abatement Cost (MAC) equals the Marginal Effluent Fee (MEF), and to pay the fee beyond that point. 3. When polluting sources with different Marginal Abatement Costs (MACs) are faced with a Marginal Effluent Fee (MEF), eachabates at a different level, which means that the effluent fee does not achieve a cost-effective solution. 4. A fertilizer tax is an example of an effluent fee. 5. Tradeable effluent permit markets can lead to cost savings as long as polluting sources face different marginal abatement costs to control the same pollutant.

Profits can be maximized by equating MR = MC = Price

A. only in discriminating monopoly markets. B. only with government price controls. C. only in monopoly markets. D. only in perfectly competitive markets.

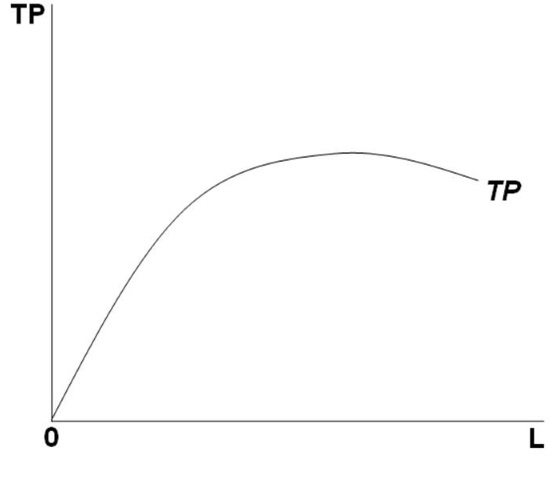

Refer to the below graph, where TP = total product and L = labor input. If this graph is for a firm that sells its product in a purely competitive market, then its marginal revenue product of labor (MRP):

A. Is constant at all levels of L

B. Increases at an increasing rate as L increases

C. Decreases as the labor input L increases

D. Increases at a decreasing rate as L increases