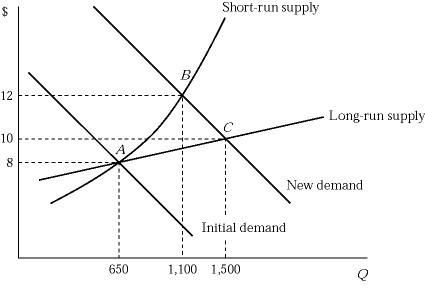

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the long run?

Figure 6.5 shows the short-run and long-run effects of an increase in demand of an industry. The market is in equilibrium at point A, where 100 identical firms produce 6 units of a product per hour. If the market demand curve shifts to the right, which of the following statements is true in the long run?

A. The market price drops below $12 as more firms enter the market and build more plants.

B. Both existing firms and new firms earn a zero economic profit.

C. All firms in the industry maximize their profits by producing the output where the marginal cost equals $10.

D. All of these are correct.

Answer: D

You might also like to view...

Which one of the following is TRUE in an open economy with a government sector?

A) The equilibrium level of real GDP occurs when total planned real expenditures equal real GDP. B) The equilibrium level of real GDP occurs when planned real investment spending is zero. C) The equilibrium level of real GDP occurs when planned real saving equals government spending. D) The equilibrium level of real GDP occurs when real net export spending equals zero.

When the Fed sells government securities, banks' reserves ________, the quantity of money ________, and the federal funds rate ________

A) decrease; decreases; falls B) decrease; increases; falls C) increase; increases; falls D) increase; decreases; rises E) decrease; decreases; rises

Monetary policy in the European Monetary Union is determined by

A) the Bundesbank. B) the European Union Senate. C) the European Central Bank. D) None of the above.

Suppose a buyer hires an interpreter who charges $5 to negotiate a deal with a seller. The buyer's valuation of the good is $50 and the seller's opportunity cost is $35 . If the net benefit to the buyer is equal to the same received by the seller, what is the price agreed upon by the two parties?

a. $42 b. $40 c. $44 d. $38