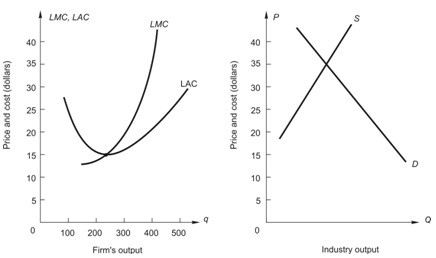

Below, the graph on the left shows long-run average and marginal cost for a typical firm in a perfectly competitive industry. The graph on the right shows demand and long-run supply for an increasing-cost industry. If this were a constant-cost industry, what would be the price when the industry gets to long-run competitive equilibrium?

If this were a constant-cost industry, what would be the price when the industry gets to long-run competitive equilibrium?

A. between $35 and $20

B. $20

C. above $35

D. $35

E. below $20

Answer: B

You might also like to view...

International capital flows strengthen

a. monetary policy and have no effect on fiscal policy. b. monetary policy but weaken fiscal policy. c. monetary and fiscal policy. d. fiscal policy but weaken monetary policy.

"The government should punish crimes and enforce voluntary agreements but not redistribute income.". This statement is most closely associated with which political philosophy?

a. liberalism b. utilitarianism c. libertarianism d. welfarism

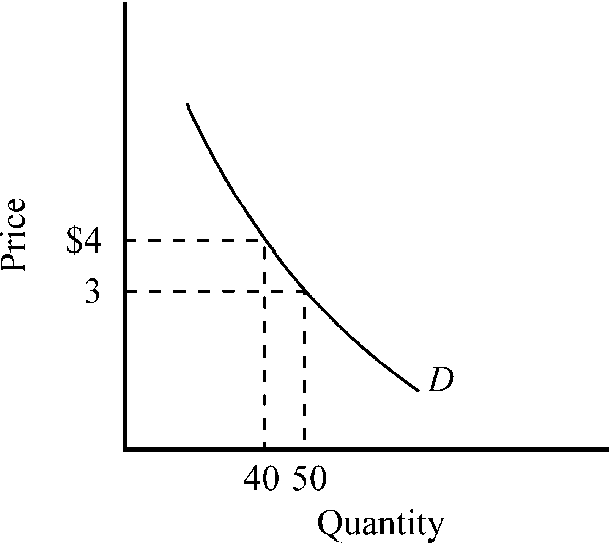

Figure 7-5

Which of the following is true for the demand curve depicted in ?

a.

In the $3 to $4 range, the price elasticity of the demand curve equals 1.

b.

At a price of $3, the price elasticity of the demand curve equals approximately -3.3.

c.

In the $3 to $4 range, the demand curve is inelastic.

d.

In the $3 to $4 range, the demand curve is elastic.

The ability to use price discrimination is ______.

a. available only to government regulated firms b. exclusive to government-owned monopolies c. available to all firms who are currently profitable d. available only to firms with market power