Answer the following statements true (T) or false (F)

1. In the long run, under conditions of perfect competition, economic profits are eventually eliminated.

2. If the entry of new firms substantially raises demand for resources, two forces tend to eliminate economic profit in the long run: upward pressure on cost and downward pressure on price.

3. The more that firms advertise, the closer they get to perfect competition.

4. The lowest possible ATC curve is attained at the optimal scale of output.

5. If price equals marginal cost at the long-run equilibrium, this means that economic efficiency is being achieved.

1. TRUE

2. TRUE

3. FALSE

4. TRUE

5. FALSE

You might also like to view...

The contribution to total revenues coming from the next worker hired is

A) marginal product. B) marginal revenue product. C) total product. D) total revenues.

Suppose that when a perfectly competitive firm produces 500 units of output a day, it earns an economic loss. If the price of each unit of output is $1.50, then, in the short run, it's clear that this firm:

A. should shut down. B. is not maximizing its profit. C. should produce more than 500 units a day. D. should not shut down if its total variable cost is less than $750.

If a firm shuts down in the short run

A) it will lose its operating costs. B) its losses will be equal to zero. C) it will incur its fixed costs. D) it will incur only its explicit costs.

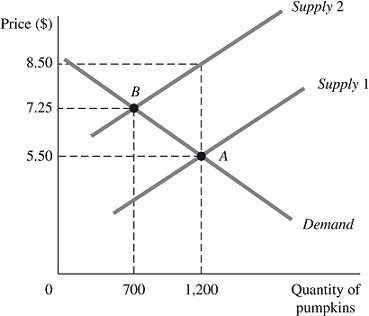

Refer to the information provided in Figure 5.7 below to answer the question(s) that follow.

Figure 5.7The above figure represents the market for pumpkins both before and after the imposition of an excise tax, which is represented by the shift of the supply curve.Refer to Figure 5.7. Had the demand for pumpkins been perfectly inelastic at Point A, the amount store owners would have received per pumpkin after the imposition and payment of this tax would have been

Figure 5.7The above figure represents the market for pumpkins both before and after the imposition of an excise tax, which is represented by the shift of the supply curve.Refer to Figure 5.7. Had the demand for pumpkins been perfectly inelastic at Point A, the amount store owners would have received per pumpkin after the imposition and payment of this tax would have been

A. $3.00. B. $5.50. C. $7.25. D. $8.50.