A perfectly competitive firm has a random marginal cost with a 20 percent chance of a high marginal cost of $20 and an 80 percent chance of a low marginal cost of $5. What is the firm's expected marginal cost?

A) $7

B) $8

C) $10

D) $12

B) $8

You might also like to view...

Which of the following is NOT a feature of monopolistic competition?

A) significant numbers of sellers in a highly competitive market B) differentiated products C) sales promotion and advertising D) inability of firms to enter or exit the market

As the price of tomatoes fell from $2.50 to $2.00, the quantity imported from Mexico fell from 1,800 tons to 900 tons. The elasticity of supply of tomatoes imported from Mexico is:

A. 5. B. 0.25. C. 3.0. D. 0.3.

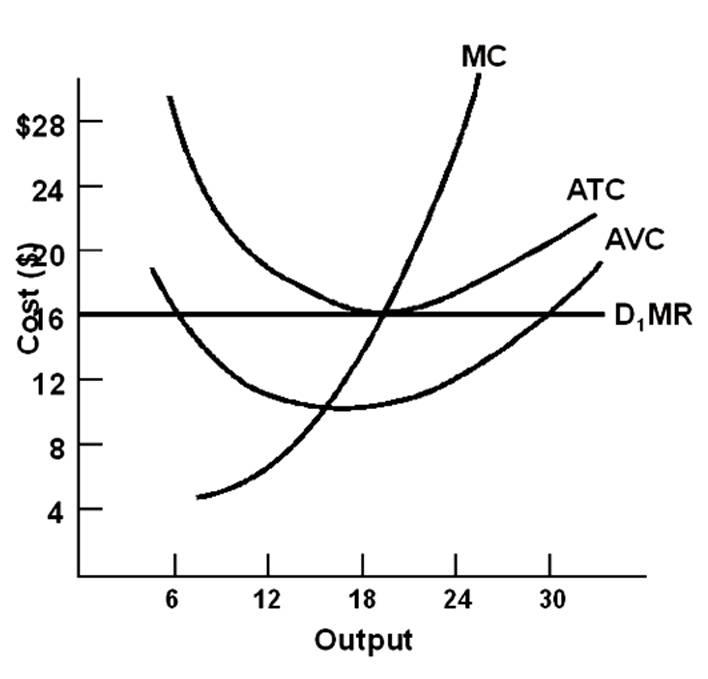

What is the lowest price the firm would accept in the short run?

Answer the following statements true (T) or false (F)

1. When an excise tax or sales tax is imposed on a product, the sellers are always able to shift the burden of the tax on to the buyers. 2. The overall tax structure of the United States is proportional or slightly regressive. 3. The state and local tax structure is largely progressive. 4. In the U.S., the progressive income-tax system substantial redistributes income. 5. In the U.S., the taxes mostly come from the rich and government spending mostly goes to programs that benefit the rich.