Because pollution taxes raise the costs of production for firms, firms:

A. will lower prices to consumers.

B. must receive a higher price at every level of output.

C. will increase the quantity produced at every price.

D. will quit producing goods that generate pollution.

Answer: B

You might also like to view...

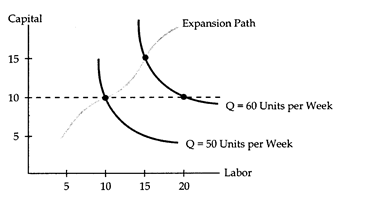

Refer to Cost of Production. The short-run total cost of producing 50 units of output per week is $180, but the long-run total cost is

The following questions refer to the diagram below. The wage rate is assumed to be $12 per hour, the rental rate is assumed to be $6 per hour, and capital is assumed to be fixed in the short run at 10 hours.

a. $180.

b. $270.

c. $300.

d. $900.

The term "market" in economics refers to

A) a group of buyers and sellers of a product and the arrangement by which they come together to trade. B) a legal institution where exchange can take place. C) an organization which sells goods and services. D) a place where money changes hands.

If in a perfectly competitive industry, the market price facing a firm is below its average total cost but above average variable cost at the output where marginal cost equals marginal revenue

A) the industry supply will not change. B) firms are breaking even. C) some existing firms will exit the industry. D) new firms are attracted to the industry.

According to new growth theory

A) physical capital is nonexcludable. B) knowledge capital is subject to increasing returns. C) knowledge capital is rival and excludable. D) knowledge capital is excludable.