Give an example of how the profits change from the short run to the long run for a firm in a perfectly competitive market.

What will be an ideal response?

but should show a thorough understanding of how profits change from the short run to the long run in a perfectly competitive market. For example, a flower producer named Bloom could be earning more than the normal rate of return in the short run, thereby making a significant economic profit. To increase her profits, Bloom buys more land to grow flowers. Other entrepreneurs who hear about the lucrative flower market will enter it. As a result, over time, the market supply curve will shift to the right as more firms enter the market and existing firms expand. The market price for flowers will decrease, eventually bringing the economic profits for Bloom and others in the market to zero.

You might also like to view...

Macroeconomics is the branch of economics that focuses on:

a. broad issues such as growth, unemployment, inflation, and trade balance. b. the actions of particular agents within the economy, like households, workers, and business firms. c. the means of production (resources and businesses) that are owned and operated by private individuals or groups of private individuals. d. workers or firms, and whether they are well suited within the overall production process.

The WTO (under the GATT agreement) provides that nations may enter into regional trade agreements as long as they:

a. limit such agreements to one. b. extend the provisions to all other nations in the WTO. c. do not jointly increase tariffs against outside countries. d. make sure they include smaller nations in their regions.

When a state government chooses to build more roads, the required resources are no longer available for spending on public education. This dilemma illustrates the concept of:

A. full employment. B. marginal analysis. C. full production. D. opportunity cost.

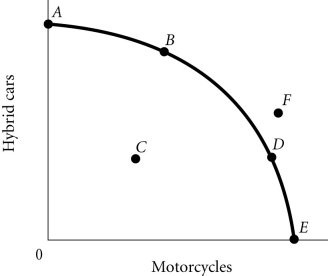

Refer to the information provided in Figure 2.4 below to answer the question(s) that follow. Figure 2.4According to Figure 2.4, as the economy moves from Point E to Point A, the opportunity cost of hybrid cars, measured in terms of motorcycles

Figure 2.4According to Figure 2.4, as the economy moves from Point E to Point A, the opportunity cost of hybrid cars, measured in terms of motorcycles

A. increases. B. initially increases, then decreases. C. decreases. D. remains constant.