An input's marginal revenue product is given by

a. the input's marginal expense times marginal revenue.

b. the input's marginal expense times the input's marginal physical productivity.

c. marginal revenue times the number of units employed.

d. the input's marginal physical productivity times marginal revenue of the firm's output.

d

You might also like to view...

________ emphasize(s) that changes in prices and interest rates are the main reasons behind fluctuations in the economy

A) The real business cycle theory B) Keynesian theory C) Ricardian theory D) Monetary theories

One reason why gold and silver have served as money is that they

a. are easy to produce. b. are easy to duplicate. c. are durable. d. All of the above are correct.

When the First Fundamental Theorem of Welfare Economics doesn't hold, there is a market failure.

A. True B. False C. Uncertain

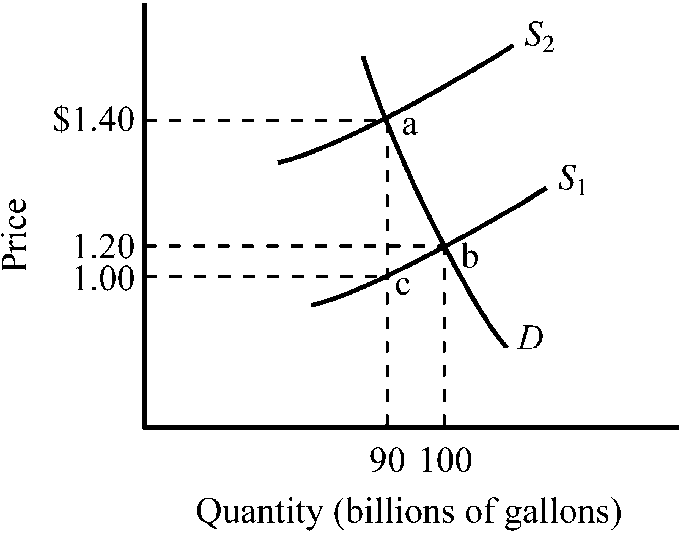

Figure 4-9

Refer to . The market for gasoline was initially in equilibrium at point b and a $.40 excise tax is illustrated. How much revenue would the $.40 gasoline tax raise?

a.

$18 million

b.

$36 million

c.

$72 million

d.

$100 million