What is a gold standard?

What will be an ideal response?

A gold standard is a monetary system in which gold backs up paper money. In a traditional gold standard, a person can present paper money to the government and receive its stated value in gold.

You might also like to view...

Empirical evidence from electric-power-producing firms suggests that

A) all electric-power-producing firms are natural monopolies. B) no electric-power-producing firms are natural monopolies. C) the largest electric-power-producing firms are natural monopolies. D) the smallest electric-power-producing firms are natural monopolies.

Which of the following statements is correct?

a. Because we have more food per capita, global food prices have decreased since 1875. b. Because we have less food per capita, global food prices have increased since 1875. c. Because we have less food per capita, global food prices have decreased since 1875. d. Because we have more food per capita, global food prices have increased since 1875.

A person's real wage will fall if the nominal wage falls, the price level rises, or both

Indicate whether the statement is true or false

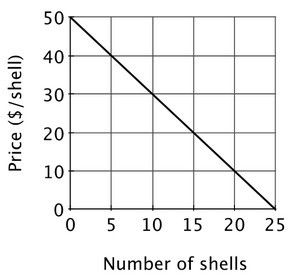

There are 20 residents in the village of Towneburg. The size of the village's annual fireworks display depends upon the number of shells that are fired off. Each resident's demand for fireworks is shown below. The total cost of the fireworks display is $1,000 plus $10 per shell. If Towneburg's fireworks display has 20 shells, then the size of the display is:

If Towneburg's fireworks display has 20 shells, then the size of the display is:

A. optimal. B. smaller than optimal. C. larger than optimal. D. unaffordable.