Which of the following statements is true of the Industrial Revolution?

A) It was a gradual process. B) It started in the capital goods industry.

C) It was a period of rapid disruption. D) It started in the United States.

A

You might also like to view...

If real GDP is $11,750 billion and aggregate hours are 175 billion, labor productivity equals

A) $23.50 per hour. B) $52 per hour. C) $67 per hour. D) $235 per hour.

The rate of production at which marginal revenue equals marginal cost is

A) a point of negative profits for the firm. B) what determines the equilibrium price in the market. C) the firm's shutdown point. D) the point where profits are maximized.

The total supply of land is:

A. upsloping. B. perfectly elastic. C. perfectly inelastic. D. greater in the short run than in the long run.

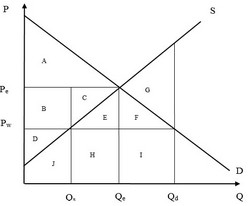

Use the following figure showing the domestic demand and supply curves for product B in a hypothetical economy to answer the next question. After trade, at a world price of Pw, consumer surplus equals area(s)

After trade, at a world price of Pw, consumer surplus equals area(s)

A. B + C + E + F. B. A. C. A + B + C + E + F. D. A + B + C + D.