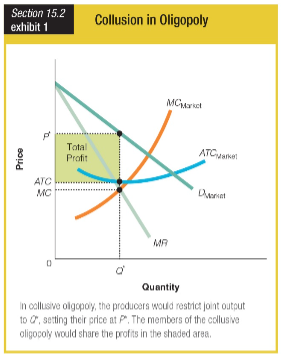

The equilibrium price and quantity are determined according to the intersection of ______.

a. the average total cost curve and the horizontal sum of the short-run marginal cost

curves for the oligopolists

b. the marginal revenue curve and the average total cost curve

c. the marginal revenue curve and the horizontal sum of the short-run marginal cost

curves for the oligopolists

d. the average total cost curve and the demand curve

c. the marginal revenue curve and the horizontal sum of the short-run marginal cost

curves for the oligopolists

You might also like to view...

In Figure 17-3 above, suppose we are working under the assumption of the Lucas model. Suddenly, monetary policy becomes more expansionary and every firm believes that the higher prices bid on their product is not being enjoyed by any other firm

We would picture this as a movement between points A) A and C. B) A and B. C) D and B. D) D and A. E) A and D.

When a paper producer pollutes the air, economists argue that there is

A) efficiency, if production is at its maximum level. B) a positive externality. C) an external cost. D) a cost paid solely by the firm.

A decrease in demand coupled with a decrease in supply results in a(n)

a. increase in equilibrium price and a decrease in equilibrium quantity b. decrease in equilibrium price and a decrease in equilibrium quantity c. increase in equilibrium price and a increase in equilibrium quantity d. ambiguous effect of equilibrium price and a decrease in equilibrium quantity e. ambiguous effect on equilibrium price and a increase in equilibrium quantity

What type of relationship do business taxes have with respect to Investment spending?

A. Constant B. Secondary C. Negative D. Positive