Which of the following is true for a perfectly competitive market in short-run equilibrium?

A. The quantity supplied equals the quantity demanded.

B. The typical firm earns zero economic profit.

C. The typical firm will always make a positive profit.

D. All of these are correct.

Answer: A

You might also like to view...

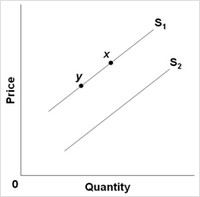

Use the figure below to answer the following question.  A movement along the supply schedule from point y to point x is associated with

A movement along the supply schedule from point y to point x is associated with

A. diminishing marginal utility. B. diminishing marginal product. C. increasing marginal product. D. increasing marginal utility.

Direct controls work only if the legal system imposes substantial penalties on violators.

Answer the following statement true (T) or false (F)

Which of the following would increase the value of a firm's stock?

a. a decrease in the firm's present profit b. a decrease in the anticipated growth rate of future profits c. an increase in the perceived riskiness of future profits d. a fall in the interest rate e. an anticipated increase in the interest rate

One of the key factors in raising people in low-income countries out of the worst kind of poverty is whether they can

a. receive unemployment compensation. b. attend college or vocational school. c. make a connection to a somewhat regular wage-paying job. d. be protected by labor laws and unions.