In the long-run, monopolistically competitive firms:

A. charge prices equal to marginal cost.

B. have excess capacity.

C. produce at the minimum of average total cost.

D. both B and C are true.

B. have excess capacity.

You might also like to view...

R2 is a statistical measure which

A) determines how important one variable is in explaining the value of another variable. B) tests the true value of a variable. C) determines how well an equation can estimate the relationship between one variable and a set of other variables. D) All of the above

When quality cannot be easily judged in advance, what provides consumers with information about the quality of a product?

a. a brand name b. a tie-in c. the quantity available for sale d. the amount of deadweight loss

An increase in productivity will:

a. Increase aggregate demand b. Increase aggregate supply c. Decrease aggregate supply and aggregate demand d. Increase aggregate supply and aggregate demand

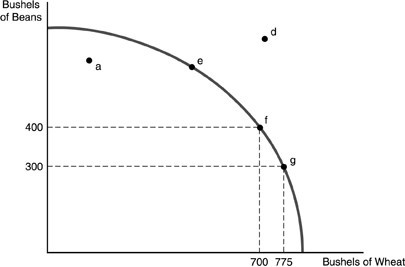

Refer to the above figure. Between points f and g, the opportunity cost of producing 75 more bushels of wheat is

Refer to the above figure. Between points f and g, the opportunity cost of producing 75 more bushels of wheat is

A. 4 bushels of beans. B. 100 bushels of beans. C. 1 bushel of beans. D. 25 bushels of beans.