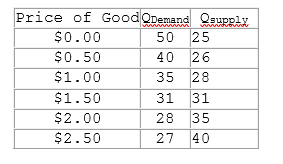

This table shows the demand and supply schedule of a good.

According to the table shown, at a price of $1.00:

A. a shortage will exist.

B. a surplus will exist.

C. more is being supplied than demanded.

D. the market is in equilibrium.

A. a shortage will exist.

You might also like to view...

A company needs to know the price of each resource it employs if it wants to determine whether or not it is achieving

A) technological efficiency. B) economic efficiency. C) accounting efficiency. D) managerial efficiency.

Which of the following statements is consistent with a decrease in supply?

A) Prices of raw material inputs have increased. B) There has been an advance in technology. C) Consumers' incomes have increased. D) The market price has decreased.

In the long run, a profit-maximizing monopolistically competitive firm sells at a price that is:

A. equal to average total cost, but higher than marginal cost. B. equal to marginal cost and marginal revenue. C. equal to average total cost, but lower than marginal cost. D. equal to demand, but higher than average total cost and marginal cost.

The selection of particular products’ production processes

A. determines the output of other products made with those inputs at the same time. B. is part of the distribution problem in an economy. C. is accomplished without regard to profit in a laissez-faire economy. D. depends upon plans for distribution of the products.