The cheapest way to produce a certain amount of output may vary between the short and long-run because:

a. all inputs can be adjusted in the long run.

b. all inputs can be adjusted in the short run.

c. input prices are fixed in the short run.

d. prices increase over the long-run.

A

You might also like to view...

A natural monopoly is one that arises from

A) patent law. B) economies of scale. C) copyright law. D) any government-imposed barrier to entry. E) mergers.

A perfectly elastic demand is one in which the:

A. demand curve is perfectly vertical. B. demand curve is perfectly horizontal. C. price elasticity is exactly 1. D. response to a change in price is immediate.

It is difficult to determine if foreign companies are selling their products for prices below their costs of production because

A) the true costs of production are difficult to calculate. B) the firms have no legal obligation to reveal this information. C) costs are calculated in the firms' local currencies. D) domestic taxes increase the firms' costs but it is difficult to determine the incidence of these taxes.

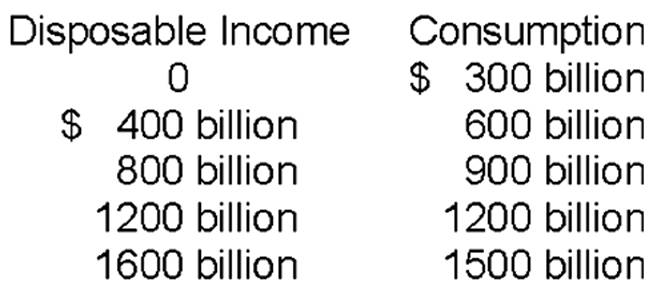

How much is the APC when disposable income is $1200 billion?