If price = marginal cost at the output produced by a perfectly competitive firm and the firm is earning an economic profit, then

A) marginal revenue is less than price. B) price exceeds average total cost.

C) total revenue equals total cost. D) average total cost is at a minimum.

B

You might also like to view...

An affordable consumption bundle is an interior choice if:

A. it lies below the budget line. B. for each good, there are affordable bundles containing a little bit more of that good and a little bit less of it. C. for each good, there are no other affordable bundles containing a little bit more of that good and a little bit less of it. D. it exhausts the consumer's income.

Are saving accounts money?

A. No, because counting saving accounts as money would double-count that money. B. No, because they technically can't be used to buy goods and services. C. Yes, because they can be used to buy goods and services. D. Yes, even though they technically can't be used to buy goods and services.

In long-run equilibrium, a monopolistically competitive producer achieves:

A. neither productive efficiency nor allocative efficiency. B. both productive efficiency and allocative efficiency. C. productive efficiency but not allocative efficiency. D. allocative efficiency but not productive efficiency.

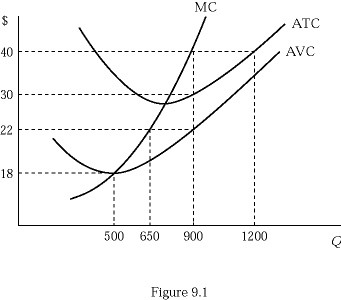

Figure 9.1 shows the cost structure of a firm in a perfectly competitive market. If the firm's fixed cost increases by 3,000 due to a new government regulation:

Figure 9.1 shows the cost structure of a firm in a perfectly competitive market. If the firm's fixed cost increases by 3,000 due to a new government regulation:

A. the marginal cost curve shifts upward. B. the average variable cost curve shifts upward. C. the average total cost curve shifts upward. D. None of these