Short-run choices imply that at least one factor of production is fixed.

Answer the following statement true (T) or false (F)

True

The short run is the period in which the quantity (and quality) of some inputs can't be changed-in other words, they are fixed.

You might also like to view...

Georgia has a MU/P of 10 for tennis lessons, a MU/P of 6 for sewing lessons, and a U/P of 2 for cooking lessons. In order to maximize utility, she should:

a. take more cooking lessons. b. take more sewing lessons. c. take more tennis lessons. d. stay with her current choices. e. take fewer lessons of each choice.

If the percentage change in price is 10%, and the percentage change in quantity supplied is 0%, then the supply for the good is

A. elastic. B. inelastic. C. perfectly inelastic. D. unit elastic.

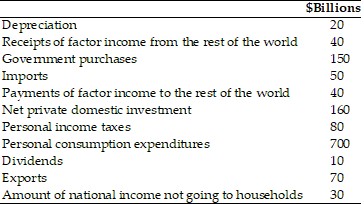

Refer to the information provided in Table 21.8 below to answer the question(s) that follow. Table 21.8 Refer to Table 21.8. The value for NNP in billions of dollars is

Refer to Table 21.8. The value for NNP in billions of dollars is

A. 970. B. 1,030. C. 1,060. D. 1,200.

Net exports is a positive number when:

A. A nation;s exports of goods and services are increasing B. A nation exports goods and services to other nations C. A nation;s exports of goods and services exceed its imports D. A nation;s exports of goods and services fall short of its imports