Aggregate demand is the sum of

a. C + I + G + (X ? IM).

b. C + I + X.

c. C + I + X ? IM.

d. C + I + G.

a

Economics

You might also like to view...

"Farm subsidies in the European Union spill over to the rest of the world." Explain this assertion

What will be an ideal response?

Economics

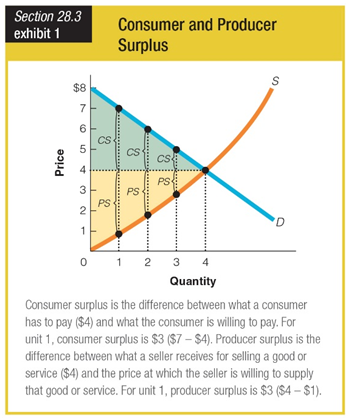

In Exhibit 1, what is the producer surplus when the price is $4 and the quantity is one?

a. $7

b. $4

c. $3

d. $1

Economics

A Keynesian model is one in which prices are sticky:

a. in the short run only. b. in the short run and in the long run. c. in the long run only. d. so that they never depend on the money supply.

Economics

The situation of oligopoly suggests

A. many firms compete in an industry. B. mergers have not occurred. C. no barriers to entry exist. D. interdependence among firms.

Economics