In the short run, ________ determines output, and in the long run ________ determines output.

A. potential output; prices

B. total spending; prices

C. potential output; total spending

D. total spending; potential output

Answer: D

You might also like to view...

Which alteration of the assumptions behind the Bertrand model can help avoid the Bertrand Paradox (that an outcome resembling perfect competition may arise with even as few as two firms)?

a. assume firms have limited capacities. b. assume firms produce differentiated rather than homogeneous products. c. assume firms play repeatedly and thus may collude. d. all of the above.

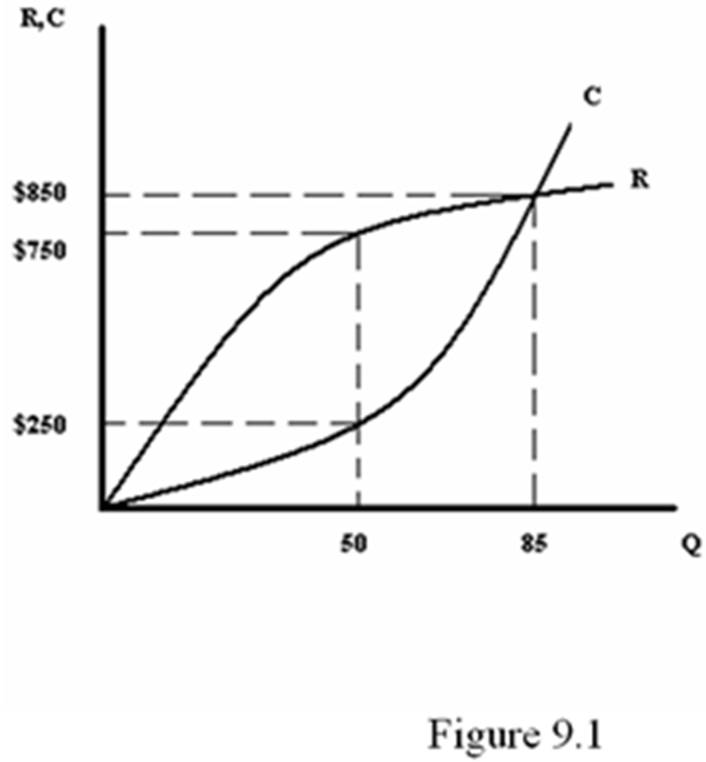

Refer to Figure 9.1. What is the maximum profit that can be achieved?

A. $250

B. $500

C. $750

D. $850

If labor supply decreases, what will happen to the real wage rate, employment, and real output, assuming no change in labor demand?

a. The real wage will increase, employment will decrease, and real output will increase. b. The real wage will decrease, employment will decrease, and real output will increase. c. The real wage will increase, employment will decrease, and real output will decrease. d. The real wage will increase, employment will increase, and real output will increase. e. The real wage will decrease, employment will increase, and real output will increase.

When calculating the costs of environmental cleanup, what factors should be taken into consideration?

What will be an ideal response?