Equilibrium price and quantity are determined by:

A. demand.

B. both supply and demand.

C. supply.

D. government regulations.

Answer: B

You might also like to view...

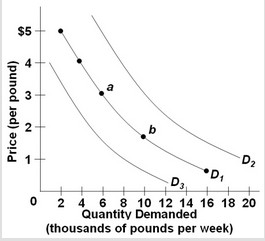

Use the following graph of the demand for coffee to answer the question below. Refer to the three demand curves for coffee and assume that coffee is a normal good. Which of the following would shift the demand for coffee from D1 to D2?

Refer to the three demand curves for coffee and assume that coffee is a normal good. Which of the following would shift the demand for coffee from D1 to D2?

A. an increase in consumer incomes B. a decrease in the price of coffee C. an increase in the price of coffee D. a decrease in consumer incomes

The tables above show the marginal costs and benefits from production of paper. If the market is perfectly competitive and unregulated, the efficient amount of paper will be produced by setting a Pigovian tax of

A) $5 per ton. B) $10 per ton. C) $20 per ton. D) $40 per ton.

For most commonly used social welfare functions, an efficient allocation is

A) always preferred over any inefficient allocation. B) not possible. C) usually preferred. D) never preferred.

In the above figure, assuming Firm 1 and Firm 2 are the sole producers in the industry, the industry quantity supplied at price P2 is equal to

A) Q1 + Q2. B) Q1 + Q3. C) Q2 + Q4. D) Q4 - Q2.